Mobile Launch Platform Market to Reach $5.2 Billion by 2030: Key Statistics and Growth Trends

The Mobile Launch Platform market has grown rapidly over the past decade due to increased satellite deployments, reusable launch vehicles, and commercial space missions. In 2022, the market was valued at $2.1 billion, reflecting a CAGR of 13.4% from 2017, when it stood at $1.0 billion. Forecasts indicate the market will reach $5.2 billion by 2030, growing at a 13.8% CAGR between 2023 and 2030.

Historical Market Trends (2015–2022)

Between 2015 and 2022, mobile launch platforms experienced steady expansion. In 2015, global revenue was $0.92 billion, increasing to $0.97 billion in 2016, a 5.4% YoY growth. By 2017, revenue reached $1.0 billion, driven by North American satellite programs. In 2018, revenue climbed to $1.18 billion, followed by $1.36 billion in 2019, reflecting 18% and 15.3% annual growth, respectively. Despite 2020 pandemic disruptions, revenue increased to $1.5 billion, and further reached $1.8 billion in 2021 and $2.1 billion in 2022.

Regional Market Analysis

North America leads the market, contributing 40% of global revenue in 2022, equal to $0.84 billion, supported by U.S. government and private aerospace investments totaling $1.3 billion in 2021. Europe contributed 28%, generating $0.588 billion, with France, Germany, and the U.K. leading adoption. Asia-Pacific is the fastest-growing region, with a 16% CAGR from 2017–2022, producing $0.42 billion in 2022, driven by India, China, and Japan. Latin America and Middle East & Africa contributed 18% and 14%, respectively.

Market Drivers and Industry Adoption

The surge in LEO satellite constellations, commercial space exploration, and defense applications drives demand for mobile launch platforms. Surveys indicate 68% of satellite operators in 2022 relied on third-party mobile launch services. Revenue from reusable launch platforms increased from $480 million in 2018 to $920 million in 2022, representing 13.5% CAGR. Leading companies, including SpaceX, Blue Origin, and Northrop Grumman, captured 42% of the market, generating $882 million in 2022. Investments in innovation rose to $370 million in 2022, up from $190 million in 2020.

Market Segmentation by Platform Type

Reconfigurable mobile launch platforms dominated the market with 58% share in 2022, equating to $1.218 billion, with a CAGR of 14% from 2018–2022. Fixed mobile platforms accounted for 42%, generating $0.882 billion, with steady adoption in mid-sized launch operators. Reconfigurable platforms are projected to reach $3.02 billion by 2030, while fixed platforms will grow to $2.18 billion, driven by demand for flexible satellite launch scheduling and rapid deployment capabilities.

Future Market Projections (2023–2030)

The mobile launch platform market is expected to expand from $2.2 billion in 2023 to $5.2 billion by 2030, reflecting a 13.8% CAGR. North America is projected to reach $2.1 billion, Europe $1.45 billion, and Asia-Pacific $1.25 billion by 2030. The number of launches utilizing mobile platforms is expected to exceed 1,050 missions by 2030, up from 480 in 2022, with YoY growth of 11.9%. Global R&D and infrastructure investments are projected to surpass $1.0 billion by 2028, up from $510 million in 2022.

Competitive Landscape

Major vendors include SpaceX, Blue Origin, Northrop Grumman, and Arianespace, holding market shares of 16%, 12%, 10%, and 8%, respectively. Revenue growth for these companies averaged 12–17% CAGR from 2018–2022. Emerging entrants focusing on modular, AI-integrated mobile platforms are expected to capture 5–7% of the market by 2030, generating $364 million in additional revenue.

Government Initiatives and Investments

Government funding and institutional initiatives significantly support mobile launch adoption. The U.S. Department of Defense allocated $480 million in 2022 for mobile launch technologies. The European Space Agency invested €250 million (~$272 million) in 2022, while Asia-Pacific governments invested $310 million between 2021–2023, supporting commercial and defense satellite launches. These programs contributed to 18–22% annual growth in government-supported missions over the past five years.

Market Challenges

High costs, ranging from $40 million–$120 million per launch depending on payload and orbit, remain a significant barrier. Integration complexity and regulatory compliance can delay project timelines by 6–12 months, especially for smaller operators. Limited availability of launch windows for LEO and GEO missions further constrains capacity and growth in emerging regions.

Conclusion

The Mobile Launch Platform market is projected to grow from $2.1 billion in 2022 to $5.2 billion by 2030, driven by LEO satellite constellations, reusable launch vehicles, and global government and commercial investments. North America remains the largest market, while Asia-Pacific shows the fastest growth. Reconfigurable mobile platforms dominated 58% of the market in 2022, and AI-integrated solutions are increasingly deployed. Historical trends, YoY growth, and projected revenues indicate strong long-term potential for mobile launch platforms across commercial, defense, and research applications.

Read Full Research Study: Mobile Launch Platform https://marketintelo.com/report/mobile-launch-platform-market

Sponsorizzato

Sponsorizzato

Categorie

Altri Articoli

The global carbon black market is witnessing a significant transformation driven by the escalating demand from the tire manufacturing and industrial rubber sectors. Carbon black, a material produced by the incomplete combustion of heavy petroleum products, serves as a vital reinforcing filler that enhances the durability, conductivity, and tensile strength of rubber and plastic products. As...

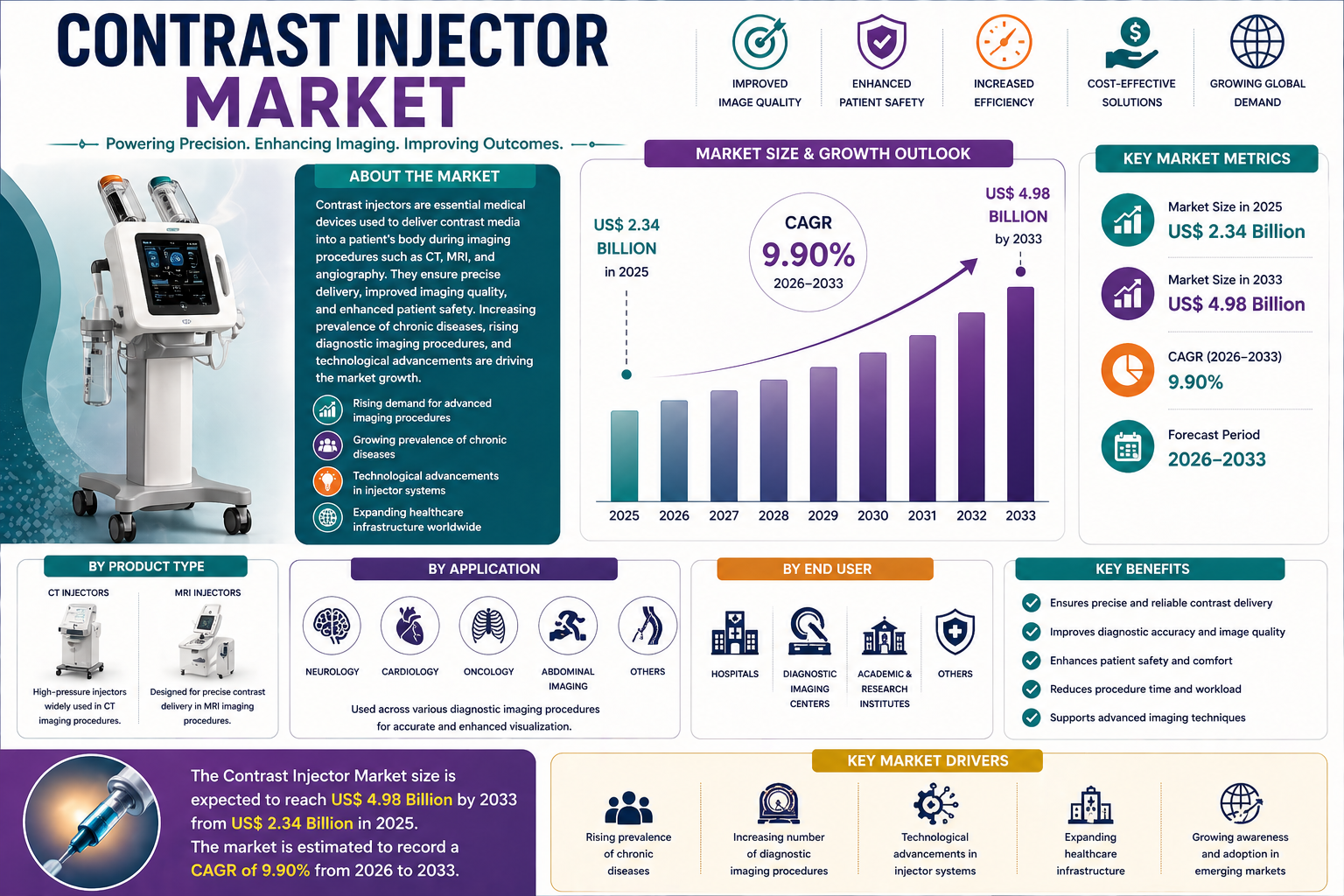

The global healthcare landscape is witnessing a significant transformation, driven by advancements in diagnostic imaging technologies and an increasing emphasis on early disease detection. Central to this evolution is the contrast injector, a sophisticated medical device used to inject contrast media into a patient’s body to enhance the visibility of tissues, blood vessels, and organs...

Square Transformer Factory refers to a specialized production environment focused on manufacturing compact electrical units used in industrial and energy systems. These components are designed to support stable voltage handling and reliable equipment operation across multiple application fields. In industrial environments, electrical stability is essential for maintaining continuous operation...

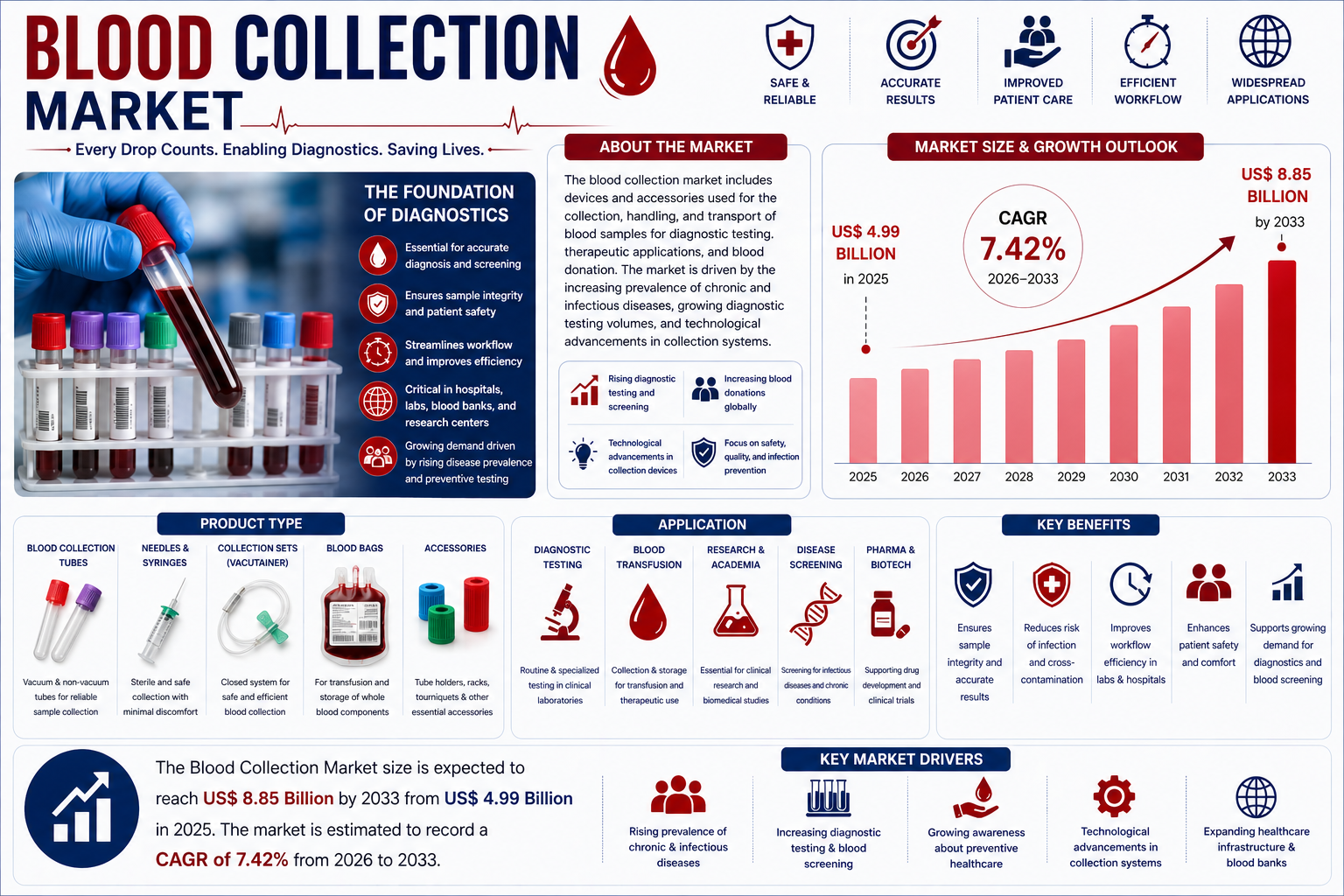

The global healthcare landscape is undergoing a significant transformation, with diagnostic accuracy becoming the cornerstone of effective patient management. At the heart of this diagnostic revolution lies the blood collection market. Blood collection is a fundamental procedure in clinical medicine, serving as the primary source for laboratory testing, blood donations, and therapeutic...